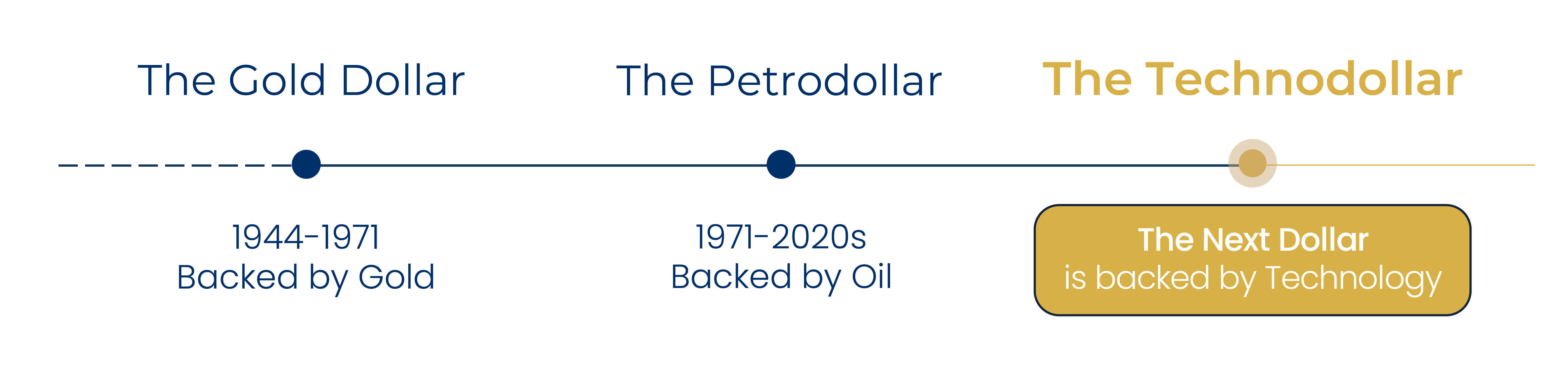

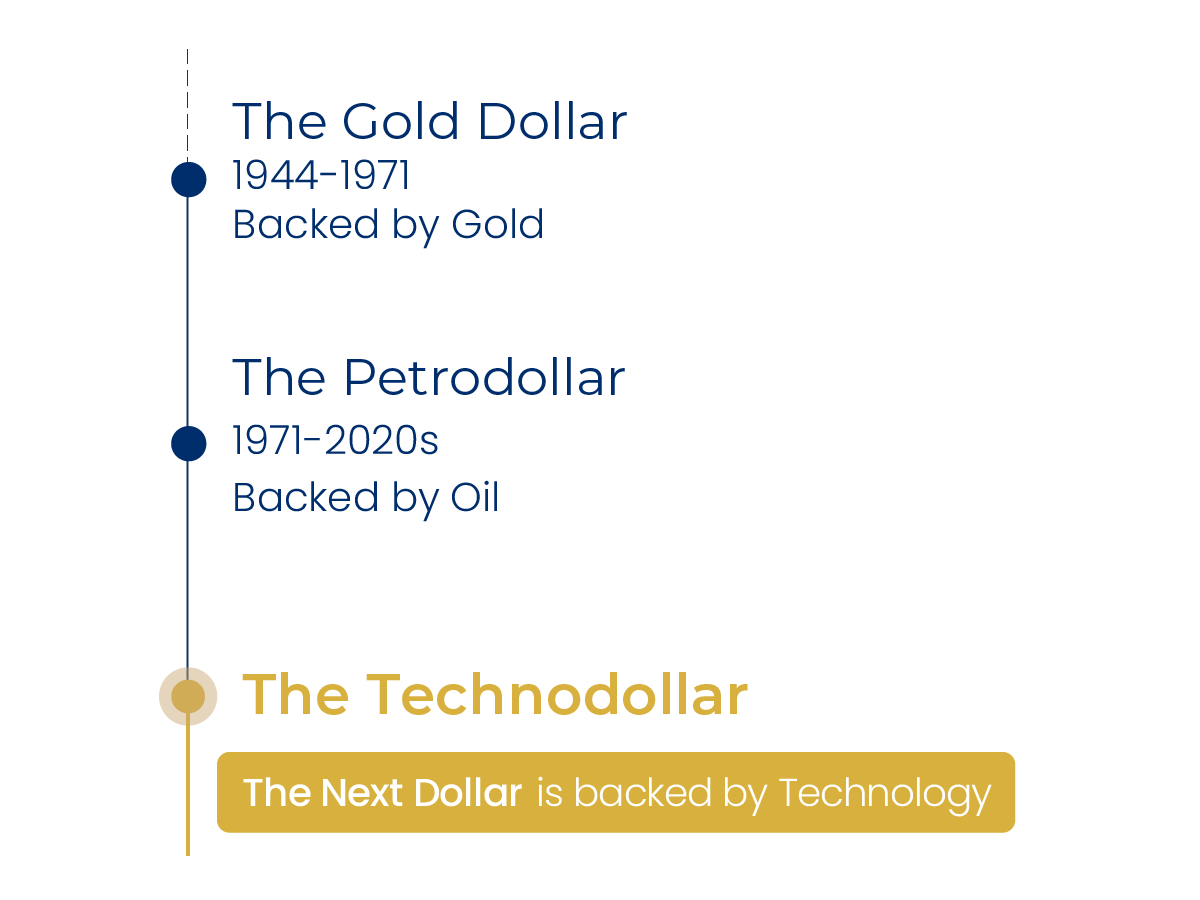

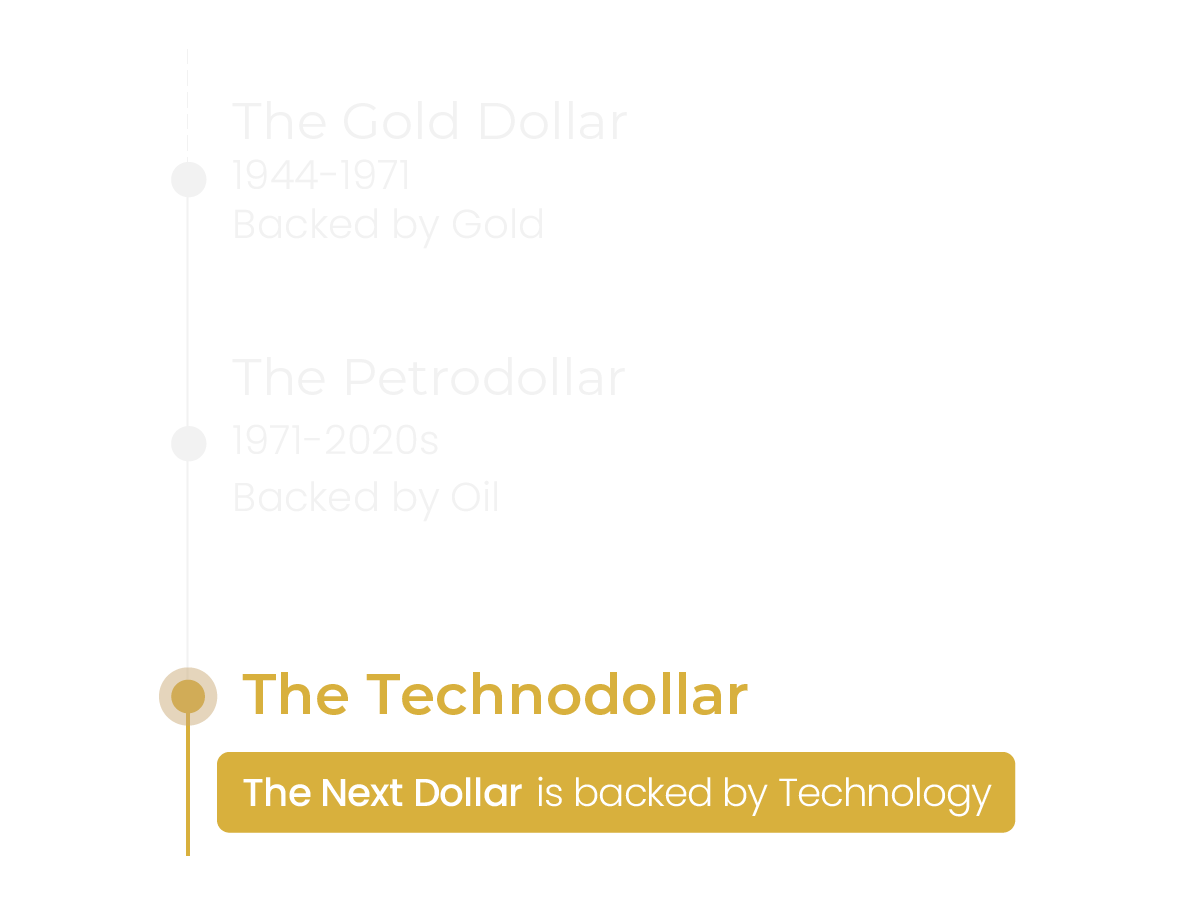

The dollar’s third form

The dollar’s third form: a regulated claim on productive American assets, built to invest in AI, run today with AI assistance under Investment Committee authority, and intended over time to move toward AI governance under human oversight.